Engineering and Construction Costs Increase at Slower Pace in April

- January 12, 2021

- Posted by: Alan Hageman

- Category: News

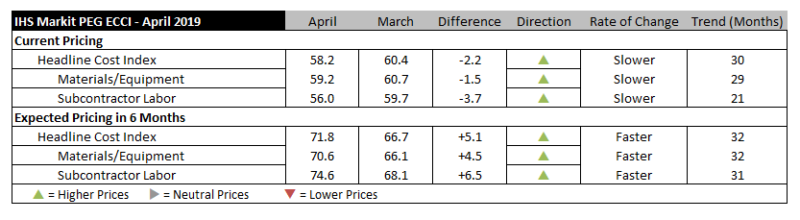

Construction costs continued to increase in April for the 30th consecutive month, according to IHS Markit and the Procurement Executives Group (PEG). The current headline IHS Markit PEG Engineering and Construction Cost Index registered 58.2 this month, a slight decline from March’s reading of 60.4. The materials and equipment price index fell to 59.2 in April with labor indexes also taking a step back in April but both remain firmly in positive territory, indicating continued price increases.

Survey respondents reported falling prices for carbon steel pipe; all other categories ranging from turbines to transportation registered price increases. The index for fabricated structural steel climbed into positive territory, indicating more reports of price increases than decreases, for the first time since November. “Fabricated structural steel prices picked up late in the first quarter due to higher raw materials costs and a seasonal pick-up in demand,” said Amanda Eglinton, principal economist, pricing and purchasing, IHS Markit. “Steel input costs will decline over the near-term, however rising labor costs and supportive demand will limit declines in prices until later in the year.”

The sub-index for current subcontractor labor costs came in at 56.0, down from 59.7 in March. Labor costs rose in all regions of the United States and stayed nearly flat in both Western and Eastern Canada.

The six-month headline expectations for construction costs index reflected increasing prices for the 32nd consecutive month. The six-month materials and equipment expectations index registered 70.6 in April after sliding to 66.1 last month. Expectations for sub-contractor labor rose to 74.6 in April, up from 68.1 in March, with labor costs expected to rise in all regions of the U.S. and Canada.

In the survey comments, respondents indicated a tight labor market for all skilled trade workers.

To learn more about the IHS Markit PEG Engineering and Construction Cost Index or to obtain the latest published insight, please click here.