Reaction to Tariffs Keep Freight Costs High

- March 4, 2021

- Posted by: Alan Hageman

- Category: News

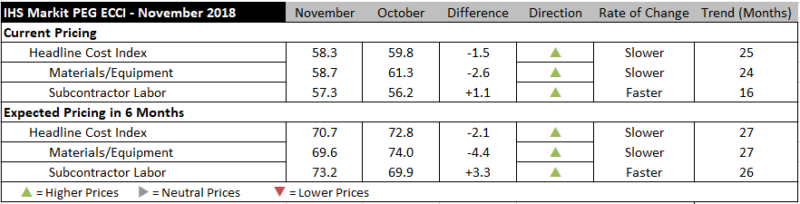

Construction costs increased once again in November, according to IHS Markit(Nasdaq: INFO) and the Procurement Executives Group (PEG). The current headline IHS Markit PEG Engineering and Construction Cost Index registered 58.3 this month, slightly lower than last month’s reading. Although prices are still rising, indicated by an index reading above 50, increases have been less widespread in the last two months.

Materials and equipment prices rose once again in November, though at a slower rate than October with the index posting 58.7, down from the October figure of 61.3. Price increases for materials and equipment were recorded in 11 of the 12 subcomponents in November; only turbines had flat pricing. Compared to last month, copper based wire and cable, heat exchangers and pumps had large gains. All other categories, although still above 50, lost some of their pricing power. The index for ocean freight transportation hit high levels in September and the diffusion index still hovers above 70.

“Shipping prices remain elevated, but some of the pressures that caused capacity strains earlier this year have partially subsided,” said Kayla Bruun, senior economist, pricing and purchasing, IHS Markit. “Over the summer, carriers cut capacity on trans-Pacific and Asia-European routes just as demand ramped up quickly and unexpectedly. The announcement of U.S. tariffs on Chinese goods caused importers to rush in shipments ahead of the implementation date, resulting in the peak shipping season moving up one month to July rather than August. Since then, volumes have retreated and carriers are keeping additional capacity available through the end of the year to accommodate any uptick in demand associated with the tariff rates increasing from 10 percent to 25 percent in January 2019.”

Current subcontractor labor prices increased at a slightly quicker pace this month, with the index reaching 57.3 from 56.2 in October. Labor costs were flat in U.S. Northeast and West but continued to increase in U.S. South and Midwest. In Canada, the Eastern part of the country registered higher labor costs, while for the West labor costs dropped.

The six-month headline expectations for construction costs index reflected expectations of increasing prices for the 27th consecutive month. The materials/equipment index fell back once more but stayed in expansion territory with a reading of 69.6. Expectations for future price increases were widespread, with all material indexes resting above 55.0. Price expectations for sub-contractor labor gained a few points and once again moved above 70. Labor costs are expected to rise in all regions of the U.S. and Canada.

In the survey comments, respondents indicated a tight labor market for all skilled trade workers as well as some tightness with regards to steel.