Uncertainty Surrounding Tariffs Driving Construction Materials Prices Higher

- May 11, 2021

- Posted by: Alan Hageman

- Category: News

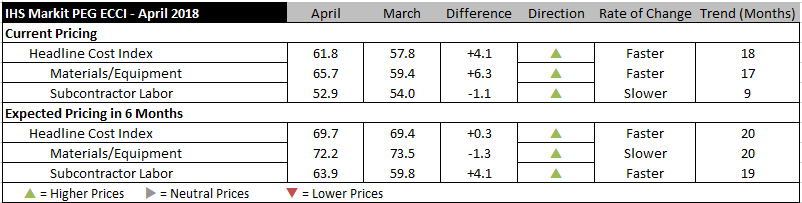

Construction costs increased for the 18th straight month in April, according to IHS Markit and the Procurement Executives Group (PEG). The current headline IHS Markit PEG Engineering and Construction Cost Index registered 61.8, 4.1 points higher than in March. Both materials/equipment and labor sub-indexes came in above 50, indicating rising prices.

Materials/equipment prices increased at a more robust pace in April; the index posted a gain of 6.3 points, reaching 65.7. Prices were up in all 12 categories. Turbines, which had registered lower prices in March, rebounded strongly this month to well above the neutral threshold of 50. The three steel categories – fabricated structural steel, carbon steel pipe, and alloy steel pipe – pushed even higher in April, indicating that steel price increases are being widely felt. Along with higher steel costs, the indexes for heat exchangers, pumps and compressors and turbines each increased by double digits in April.

“Steel buyers seem paralyzed by the uncertainty around 232 and 301 tariffs: when the cost is unknowable and availability is dubious, rational behavior is to do nothing,” said John Anton, associate director – pricing and purchasing, IHS Markit. “Hopefully, clarity will come by May 1, the due date for a decision on country exemptions.”

Current subcontractor labor index expanded at a slower rate this month compared to last; the index dropped 1.1 points to 52.9, marking the ninth straight month of increasing prices. Labor costs continued to increase in all U.S. regions. After no change in March, the labor cost index for Western Canada moved into positive territory while the index for Eastern Canada fell into negative territory in April.

The six-month headline expectations for construction costs increased for the 20th consecutive month: the index moved up 0.3 points to 69.7. The materials/equipment index remains elevated at 72.2, despite a drop of 1.3 points this month. Expectations for future price increases were widespread, with index figures for every component well above neutral. Price expectations for sub-contractor labor came in at 63.9, a 4.1-point climb from March’s 59.8. Labor costs are expected to rise in all regions of the U.S. and Canada.

In the survey comments, respondents indicated an expectation of a shortage of electrical engineers, welders, and carpenters in 2018. They also continued to highlight concerns about the uncertainty around developments in U.S. trade policy.

To learn more about the IHS Markit PEG Engineering and Construction Cost Index or to obtain the latest published insight, please click here.